I design Tokenomics. Here is what I have learned. (Part I)

I design Tokenomics. Here is what I have learned. (Part I)

Well, I don’t “only” design Tokenomics. I do research at an L1 so this is also part of my job. You get the idea. While I can’t discuss any details of ongoing product-related development, I can definitely share the lessons I have learned to try and build a compelling and meaningful economic model. What started as a nice little project together with a couple of super brilliant dorks at Zilliqa transformed me into a rabbit-hole visiting weirdo that reads about niche economic theories on my lunch break. ADHD is helluva drug.

This article series will cover some general Tokenomics principles, the main problems that protocols face when their token is live in the wild and potential solutions or at the very least, the general direction in which I see Tokenomics design heading. I also keep the discussion at a high level due to the fact that Tokenomics is a new science (?) that is challenging fundamental principles which we all thought were set in stone. Things like scarcity value, distribution, intrinsic value, etc. Without further ado, let’s jump in!

But first, what are Tokenomics?

Crypto uses tokens. The fact that everybody can freely own and trade them without (for the most part) a central bank or specific regulation is a neat new thing. People trade stuff between each other all the time. This is called “the economy”. Tokens + economics = tokenomics. There, who needs fancy Investopedia-style definitions? You will sometimes see the term Tokenomics refer simply to the token distribution strategy and percentages during, after and before launches. While that is definitely part of it, Tokenomics have evolved a lot in the past couple of years as areas in crypto such as DeFi and gaming have started to mature.

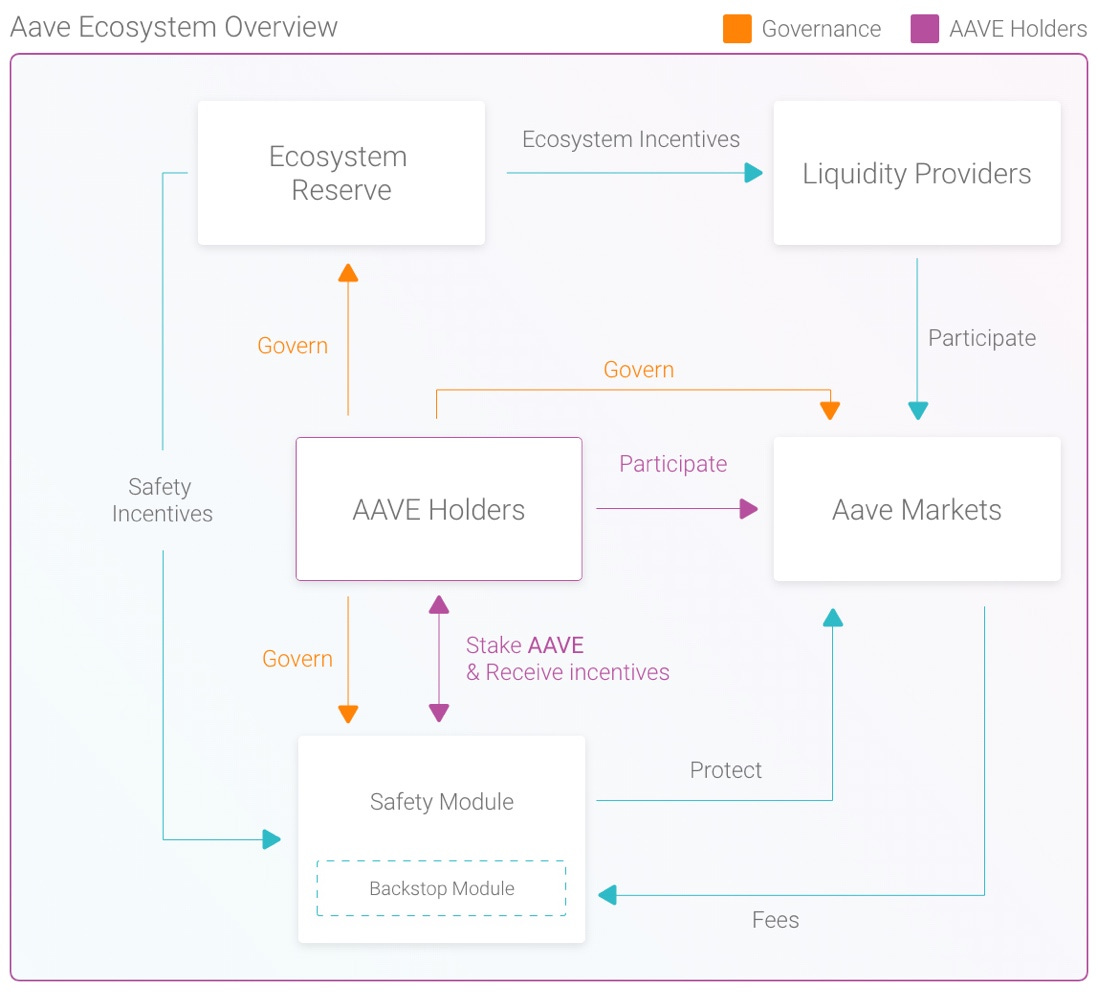

Tokenomics design mostly means the entire economic ecosystem of one or several tokens. AAVE’s token distribution, interest rate model, LTV ratio and risk parameters? Tokenomics. Axie Infinity’s AXS shards, governance and economy loop? Tokenomics. The Sandbox’s SAND distribution, land sales and asset minting strategy? That’s Tokenomics. Basically, in any crypto project, the economy part + all the other use case documents and marketing proposals form the whitepaper.

Getting the tokenomics of your project right before launch is arguably the most important part of making sure that your GameFi project or DeFi protocol will be at least somewhat sustainable and won’t dump into oblivion. I will go more in detail on what are the causes of this later on.

Arguably the thing through which protocols live and die the most has something to do with good, bad or unforseen tokenomic design. Making a web interface for a smart contract isn’t that terribly difficult. Security is, but that is another topic for another time. What is difficult however, is competing with other protocols with increasingly interesting reward mechanisms so that the whales in your ecosystem don’t sell your token’s market cap through the floor.

Another aspect to remember is that we are talking about blockchain-based assets. If you own the keys, you own the asset. No judge, central bank or ahem…Treasury Department can confiscate assets without the owner giving up their private keys. That goes for AMMs as well. Unless through fraudulent design, user’s can’t have their tokens locked without their consent and they are free to do with them as they please. Your job, if you design a digital and free economic model, is to incentivize people to stay within your ecosystem and be active.

Lesson 1: Everybody is a Degen

Yes, including you, your grandma, her ex from primary school and including (and maybe especially) your smug investment banker friend. Human beings are incentive-based animals to their core. We want more good things and less bad things. Drug dealers risk their freedom because they can make a lot of money in order to buy nice stuff. Hypothetically not many people would accept working 16 hours a day seven days a week for half of minimum wage. The time to reward ratio is very bad, therefore discouraging. Behavioral economics is not a new thing and the exact same principles apply in crypto.

Let’s say Bob likes DeFi and builds an AMM DEX. He wants people like Lisa with $1000 to hop in as well as millionaire Jennifer. He provides staking rewards, does stuff like APY boosts in yield farms and benefits for active governance participation in order to do two things: 1. Make Lisa and Jennifer join; 2. Make Lisa and Jennifer stay. However, John has also built an AMM DEX. It offers better rewards because he managed to bring in more people than Bob, supports more coins and also offers borrow/lend features. Both Lisa and Jennifer take out their money from Bob’s protocol and move to John’s to get the better early APYs and benefit from the increased utility.

This is called mercenary liquidity and is something that every tokenomics designer has to understand and account for. Lisa and Jennifer will eventually take all or most of their funds and migrate. It’s a free country… ugh I mean network. The whole gist is to make them stay as long as possible and be as active as possible. Bob makes a profit through the fees his protocol gets for example and Lisa and Jennifer by providing liquidity, staking, etc. But if it’s all for naught and users eventually leave, why build anything really? That takes us to:

Lesson 2: It’s a Zero-sum game

All of it. Not just crypto. The stock-market is fundamentally a Zero-sum game. Investors that get in early on projects make massive profits due to the fact that other people see the utility/hype later than they did. Which makes the company/protocol/asset more desired, therefore more valuable. Early investors sell their assets to other willing buyers at fair market price. The willing buyers hope/think that the underlying asset will appreciate even more in the future, therefore justifying its purchase for more than it was worth let’s say a year ago. In order for the seller to make a profit, the buyer needs to purchase the asset and be comfortable to take on the risk of it depreciating against the potential of it being more valuable in the future.

In simpler words, in order for one person to win something, another person needs to lose something. That is the definition of a zero-sum game. The seller loses higher future potential earnings and the seller loses his funds and takes on risk. Zoomed out enough, most investment activity looks not too dissimilar from a literal ponzi scheme. Buy low, sell high and all that.

That being said, this isn’t really a bad thing in and of itself. Society is forever changing and the economy alongside it. Some stuff and services that have been valuable in the post are no longer worth anything today and vice versa. The only constant is change, that is as much true in investing as it is in physics. And although crypto and private equity markets have been very much correlated these past years, there is a notable difference between these two markets: Life cycle.

Crypto has much faster market cycles. Meaning we go from a low steady price to a bull market all-time high to a market crash to a low steady price much faster than we do in the stock market. Crypto had arguably three market cycles: October 2013 - May 2014; March 2017 - October 2018 and October 2020 - April 2022. The latest private equity bull market, the longest in history, has been going on since 2010 and we are arguably still in it. This makes many crypto projects and protocols have much faster life-spans, which in turn forces projects to make more compelling economic ecosystems faster. Take the good with the bad.

When you look at it this way, mercenary liquidity doesn’t seem like such an evil thing anymore. It simply is a phenomenon that has to be taken into consideration when designing Tokenomics. Nothing lasts forever, so you should best try to incentivize people to stay as long as possible. I feel that we are only scratching the surface with this really. User retention features that come to mind are for example locking mechanisms similar to CRV and veCRV. By locking their tokens for a set amount of time, users get bigger rewards. This system has a flaw though, the fact that most users sell their tokens once they are unlocked. It does function a lot better in already established platforms with a lot of TVL like Curve than it does on smaller protocols.

Another interesting approach comes from GameFi and the most popular P2E trading card game, Splinterlands. Instead of doing constant airdrops that are subject to pump and dumps, the game incentivizes players to stake their SPS tokens for chances at daily rewards. This is somewhat loosely similar to the concept of lottery savings. This system is a lot better than a classic airdrop because it mitigates two problems:

First, rewards dumping sell pressure. By not dropping for example 1% of your total tokens to users all at once only to have the majority sell them off all at once, sell pressure is much less of a problem. Second, mercenary liquidity is discouraged further. Players have an incentive to keep at least part of their assets within the game to get that constant chance at having a rare card drop. You make it long-term economically viable for the player to keep assets in while not turning your coin into a farm token. Food for thought for applications in DeFi.